Two in every five university leaders say they have adequate resourcing in place to deliver internationalisation strategies, despite it being a high priority at institutions, new research has suggested.

The Thriving in a hyper-competitive world report, published by international management consultancy Nous Group and global education provider Navitas, found that 90% of more than 100 senior international education and global engagement leaders at universities in Australia, the UK and Canada said internationalisation was high on the agenda.

More than three quarters stated it was well supported across senior levels of their institution, but resources are lacking. It also suggested that the higher education sector is preparing for a period of “hyper competition”.

Strategies to internationalise universities are also becoming more complex, with the pandemic creating the need to diversify approaches and investigate new ways of engaging with students and deliver learning across closed borders, Nous principal, Matt Durnin, said.

“Today internationalisation includes affiliations and partnerships, transnational education and offshore brand campuses, however, international student recruitment is still the most important area of focus for university leaders due to its pivotal role in revenue generation,” he explained.

Photo: Navitas/ Nous

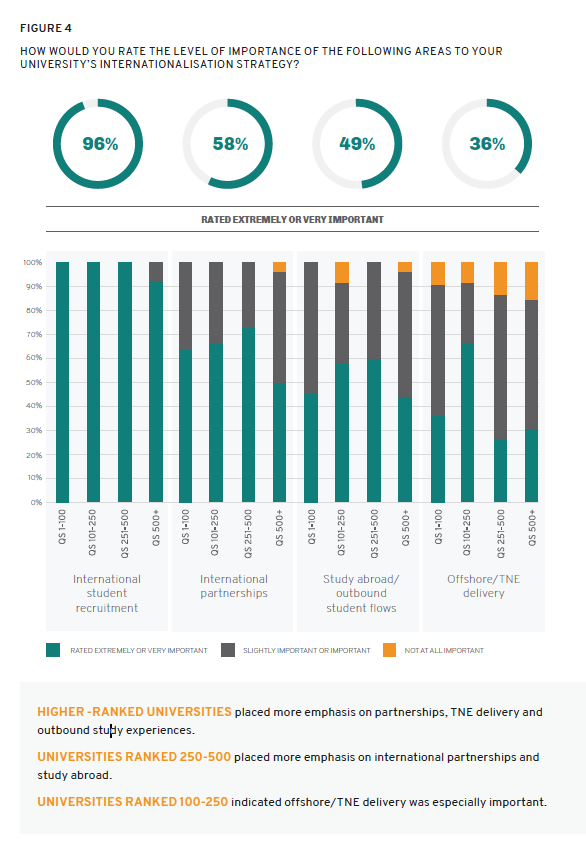

A total of 96% of respondents rated international student recruitment as very or extremely important to their internationalisation strategy.

The same proportion indicated competition to recruit international students over the next three years will be higher or much higher than pre-pandemic levels.

The report also suggested that higher-ranked institutions tended to place more importance on partnership – such as articulation agreements with other universities – TNE delivery and outbound study experiences, while those ranked 100-250 indicated offshore/TNE delivery was “especially important”.

Universities ranked from 250-500 placed more emphasis on international partnerships and study abroad, it added. Priority focus areas were generally similar across the three countries, although Canadian respondents gave much lower importance to offshore/TNE delivery, the report noted.

Navitas global head of Insights and Analytics Jon Chew also pointed to the availability of scholarships and the “keenness to invest”.

“You get almost that textbook step shape pattern where the highest ranked side invest the most and the lowest ranked either plan to or are able to in the foreseeable future, invest less,” he told The PIE.

The report urged universities to develop not only sophisticated pricing strategies but also sophisticated scholarships strategies.

Across the three countries survey, 67% of QS 1-100 institutions said they planned to invest more in scholarships, while 55% of those ranked 101-250 indicated they planned to invest more or much more.

The move is linked to diversity agendas, with the report noting that while Chinese students have typically had a lesser need for scholarships to fund international study, new core and emerging markets like India and Nigeria are far more price sensitive.

“Given that higher-ranked universities have higher sticker prices, they will need to invest more in scholarships to compete on price,” the report said. On the other hand, lower-ranking institutions plan to reduce investment in scholarships in recognition that “discounting won’t result in increased volumes”.

“Universities are now discovering they can apply different discounts in different markets, targeting discounting strategies where they will add most value,” it added.

Chew suggested that high-ranking institutions may be able to focus on diversification, TNE, study abroad and scholarships, “lower- and middle-ranked really just have to knuckle down and get student recruitment”.

“Historically we’ve seen middle- and lower-ranked institutions be much more dependent on transnational education and articulation for recruitment than high risk universities. We have seen that flip in the pandemic in terms of interest,” Durnin added.

The finding are likely to be universal and extend to countries not surveyed, the experts continued.

“Certainly in many of the major English-speaking countries have got that phenomena,” Chew continued, especially when it comes down to competition.

“We like to say that global demand for international education will grow on our modelling about 4.5% a year for the foreseeable future, for the next 10 years or so. And you would have to think supply is going to grow faster than that.”

Both Chew and Durnin also pointed to the balancing act international leaders are facing.

“In the face of significant external challenges and internal constraints, international education leaders need to make strategic decisions around key areas of focus, investment priorities and partnerships,” Chew said.

“We’ve seen a lot of institutions start to perhaps prematurely turn their back on the Chinese market”

International education leaders have to navigate three things, Chew suggested – big internationalisation agenda, increasing student needs and then growing competition.

“You want to grow and be more international, diversify, look after the students and make sure that the university down the street doesn’t eat your lunch. In the middle of all that, you’ve got the limited capability and resourcing issues. It’s a real juggle almost this infinite need and finite resources that you’ve really got to balance.”

Durnin added that institutions focusing on diversifying international source countries will need to acknowledge that agenda will “raise per student acquisition costs”.

While aggregators have managed to deliver in markets where institutions are underrepresented, according to Durnin, there is no shortcut to diversification, the pair agreed.

“You’re trying to crack a new market segment and in some cases you might be going into places that maybe haven’t even thought of international education as an option,” Chew continued.

“You just have to work hard to get that sort of brand presence and become top of mind and become known and preferred as an option.”

Once markets have matured, there are options to build success further, such as through fairs, loyal agents, but for new markets “there’s no quick fix”, Chew said.

“It’s heartening, I think, in the results to see [diversification] as being one of the top investment areas because, a lot of institutions have been talking about it for a long time but I don’t think we’ve seen that willingness to invest to actually achieve that,” he added.

Durnin also warned that some institutions have been too quick to shift away from China.

“We have a narrative that if you’re outside of the top 200, China is a very difficult market and students aren’t going to apply outside of the top 200 institutions. And we’ve seen a lot of institutions start to perhaps prematurely turn their back on the market,” he said.

“While we do see some signs that overall outbound mobility from China could plateau, there are a lot of reasons to be bullish on the market, at least in the near to medium term. If you look at that over-saturation of Chinese students in the top 200 and the diversification agenda, there’s going to be unmet demand in China. So it’s way too early for universities from say that 200 to 400 range to turn their back on the market.”

The post “Hyper-competition” period approaches but institutions missing adequate resources appeared first on The PIE News.